Answer the question

In order to leave comments, you need to log in

How to use nuclear regression for forecasting?

Hello.

Two independent subtasks. There is data. It is necessary:

1) "Smooth" the row;

2) Predict

Everything using kernel regression.

I perform smoothing using the Nadaraya-Watson formula, the Gaussian kernel. Everything is working.

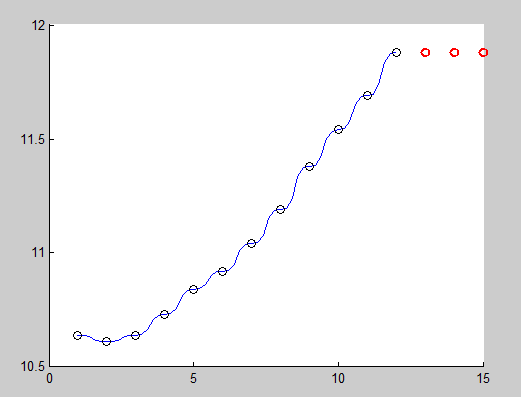

I predict with the same formula - trouble. All values are equal (in red):

What am I doing wrong?

UPD:

% Код для сглаживания

function [ yy_smooth ] = kernel_smoother( xx, yy, xx_smooth, h )

yy_smooth(1:numel(xx_smooth)) = nan;

kernel = @(x0,x) exp(-(x0-x).^2 / 0.5 / h^2);

n = numel(yy);

% Evaluating yy_smooth

function yhat = y(x0)

numerator = 0;

denominator = 0;

for i = 1:n

ker_x0xi = kernel(x0,xx(i))*yy(i);

numerator = numerator + (ker_x0xi * yy(i));

denominator = denominator + ker_x0xi;

end

yhat = numerator/denominator;

end

% Filling yy_smooth vector

for j = 1:numel(xx_smooth)

yy_smooth(j) = y(xx_smooth(j));

end

end

% --------------------------

% Код для прогнозирования

% 'p' -- порядок регрессионной зависимости, т.е. сколько предыдущих значений используется для прогноза

function [ yy_forecast ] = kernel_forecaster( xx, yy, xx_forecast, h, p )

yy_forecast = [];

for xi = xx_forecast

xx = xx((end-p):end);

yy = yy((end-p):end);

yy_forecast = [...

yy_forecast, ...

kernel_smoother(xx,yy,xi,h)];

xx = [xx, xi];

yy = [yy, yy_forecast(end)];

end

end

% --------------------------

%Само использование

y = [10.64 10.61 10.64 10.73 10.84 10.92 11.04 11.19 11.38 11.54 11.69 11.88];

x = 1:numel(y);

xx_smoothed = 1:0.2:numel(y);

xx_forecast = x(end)+1:1:x(end)+3;

yy_smoothed = kernel_smoother(x, y, xx_smoothed, 0.7);

yy_forecast = kernel_forecaster(x,y,xx_forecast, 0.7, 4);

%Дальше идет простая визуализацияAnswer the question

In order to leave comments, you need to log in

Your forecast is clearly not moving, it is frozen at the last value.

Didn't find what you were looking for?

Ask your questionAsk a Question

731 491 924 answers to any question